Investing in tax liens is a niche real estate strategy where returns are often set by law, and entry costs can be relatively low in some markets. Actual results depend on the state, the auction format, and when the owner redeems.

That said, it’s also widely misunderstood due to its complexity, and it can involve various risks. For real estate professionals, understanding how tax lien investing works can help diversify investment strategies and avoid common pitfalls.

This guide explains what tax liens are, how tax lien investing works, the benefits and risks involved, and how to get started.

What is a Tax Lien?

A tax lien is a legal claim that a local government records when a property owner does not pay property taxes. The lien represents the unpaid tax balance plus any interest, penalties, and fees allowed by that jurisdiction.

Owning a tax lien is not the same as owning real estate. A lien gives you the right to collect what is owed under state and local rules. The property is collateral for the debt, but you do not control the property simply because you hold the lien certificate.

Counties and municipalities sell tax liens to bring in revenue without waiting for delinquent owners to pay. When an investor buys the lien, the investor pays the overdue amount to the county. The owner clears the lien by redeeming through the county, which then sends the investor the principal plus the allowed interest and fees.

Some states sell tax lien certificates, while others sell tax deeds. In tax lien states, investors are buying the right to collect unpaid taxes, not the property itself. In tax deed states, the government sells ownership of the property, often through a different auction process. The rights an investor receives depend entirely on state law, so it is essential to know which system your market uses before getting involved.

How Tax Lien Investing Works

Tax lien investing follows a legal and administrative process that is driven by state and local law. Understanding each phase can help real estate professionals evaluate risk, timing, and realistic outcomes. Generally, here's how it works:

Property Taxes Become Delinquent

The process begins when a property owner fails to pay property taxes by the required deadline. After a grace period, the taxing authority classifies the taxes as delinquent. Interest, penalties, and administrative fees may start to accrue at this point.

Local governments depend on property tax revenue to fund essential services. Rather than waiting indefinitely for payment, many jurisdictions take action to recover the unpaid amount.

The Tax Lien is Created

Once taxes are delinquent, the county or municipality records a tax lien against the property. This lien represents the government's legal claim for the unpaid taxes and associated charges.

The lien attaches to the property itself, not the owner. If the property is sold, refinanced, or transferred, the lien must typically be satisfied before a clear title can pass.

The County Sells the Tax Lien to Investors

To recover revenue quickly, many counties sell tax liens to private investors through public auctions. These auctions may take place online or in person and are governed by state law. However, not all states allow this.

Auction formats can vary. Some states use interest rate bidding, where investors compete by accepting lower returns. Other states use premium bidding, where investors pay more than the lien amount, with the interest rate remaining fixed. In some jurisdictions, liens are assigned through a noncompetitive process, depending on local rules.

In an interest rate bidding state, investors compete by accepting a lower rate, so the winner may earn less than the maximum allowed by law. In a premium bidding state, the interest rate stays fixed, but the investor pays extra upfront to win the lien. Paying more up front can reduce your real return if the lien redeems quickly.

When an investor wins a bid, the investor pays the delinquent tax amount to the county. In return, the investor receives a tax lien certificate or similar instrument that documents the claim. In some places, lien certificates can also be assigned or sold to another investor. Rules vary widely, so investors should confirm whether transfers are allowed in that jurisdiction.

The Redemption Period Begins

After the lien is sold, the property owner enters a redemption period. This is a legally defined window during which the owner can repay the delinquent taxes. In many places, the redemption window is often around one to three years, but it depends on the state and sometimes the county. Depending on the county, you may be required to send written notices to the owner after you buy the lien and again when the redemption period ends.

To redeem the lien, the owner must pay the original tax amount plus interest, penalties, and fees as allowed by law. The payment is typically processed through the county, which then forwards the investor's principal and return.

Redemption periods vary widely. Some states allow redemption in as little as a few months, while others allow multiple years. During this time, the investor cannot take possession of the property.

Tax lien certificates usually come with time limits. If a lien is not redeemed, the investor must take action within a specific window to preserve their rights. Missing that window can weaken the claim or cause the lien to expire, so it's important to track accordingly.

Investor Returns Are Earned Through Redemption

It’s common that tax lien deals will end with the homeowner paying what they owe. When that happens, you get your money back plus the interest and fees the law allows.

Some owners pay quickly, and some may wait until the last minute. If your money is tied up for a longer period, your real return for the year can end up lower than the rate you saw advertised.

What Happens if the Owner Does Not Redeem

If the redemption period expires without payment, the investor may gain the right to pursue foreclosure. This doesn’t happen automatically, and the investor must follow strict legal steps that are defined by state law. Foreclosure requirements often include additional notices, waiting periods, and court filings. The process can take months or longer and may involve legal and administrative costs.

If foreclosure is completed successfully, the investor may obtain ownership of the property or the right to sell it. Generally, foreclosure is not common for most liens, as many owners resolve the debt before it reaches that stage. When foreclosure does happen, it often involves vacant land or distressed properties rather than occupied homes.

Property Research Impacts Lien Risk

Even though tax lien investing starts with a debt claim, the underlying property always matters. If foreclosure becomes necessary, the value, condition, and marketability of the property will determine whether the investment is profitable.

This is why experienced investors treat tax lien selection like real estate underwriting. Location, property type, neighborhood demand, and physical condition all influence risk, even before a bid is placed.

Important Considerations of Tax Lien Investing

-

State laws and auction rules: Tax lien laws differ significantly by state. Some states cap interest rates, while others allow competitive bidding that drives returns down. Certain states use premium bidding, where investors pay more than the lien value, which can impact profitability.

-

Property research: Not all liens are attached to desirable properties. Investors must research location, property condition, zoning, occupancy status, and market value. A lien on a landlocked or environmentally contaminated property can become a costly mistake.

-

Senior liens: Property tax liens are often paid first, even ahead of mortgages, but lien priority can still be complicated depending on the property and local rules. Check the local statutes and the property’s title details before bidding.

-

Capital lockup: Funds are tied up for the duration of the redemption period. Investors cannot access their capital until the lien is redeemed or foreclosure is completed. In some markets, investors also choose to pay future property taxes while they are waiting, so no one else buys a newer lien on the same property. That can increase the total cash you have tied up.

-

Ongoing responsibility: Investors need to monitor redemption timelines, review notices, and decide when to take the next legal step if payment does not arrive. While it doesn’t involve managing tenants or repairs, it still requires attention and follow-through.

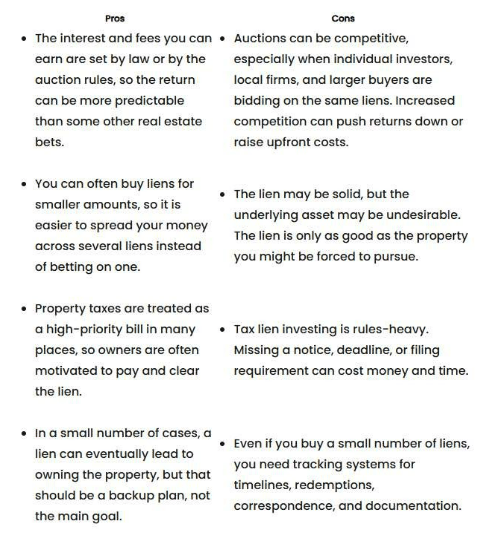

Pros and Cons of Tax Lien Investing

How to Invest in Tax Liens

Investing in tax liens can be a rather complicated process. Outlined below is generally what you can expect when getting started:

Step 1: Choose ONE Market and Learn the Rules

Start by learning local rules. Learn the auction rules, redemption period, interest structure, and foreclosure requirements before you make any moves or start bidding. It is also a good idea to confirm registration requirements, deposits, and auction schedules directly with the county before auction day.

Step 2: Build a Screening Checklist

-

Market value ranges from comps or assessment

-

Property type and location demand

-

Occupancy indicators

-

Physical condition signals, if available

-

Prior sale history

Step 3: Set Your Bid Limits in Advance

Before the auction starts, decide the lowest return you are willing to accept and the most extra money you are willing to pay above the tax amount, if that county allows premium bidding. If the numbers don't work, it's okay to skip the lien.

Step 4: Confirm Your Tracking System

-

Certificate numbers and purchase dates

-

Redemption deadlines

-

Required notices and timing

-

Expected payoff if redeemed at different points

-

Foreclosure cost estimates, if needed

Step 5: Plan for Both Outcomes

Have a redemption plan and a foreclosure plan. Most of the time, your return comes from redemption. However, your foreclosure plan should be there in case the owner does not redeem.

Step 6: Use Specialists When the Situation Calls for It

For liens that move toward foreclosure, use local counsel and, when appropriate, title support. Tax foreclosure has strict rules, so it helps to follow a clear, local process.